Confessions of a Former Retail Lender — #2

“Good luck making over 200 bps while staying competitive on rate.”

My parting message from my old SVP when I left retail. Funny story, he was the one who declined my PE request days prior, which prompted my switch.

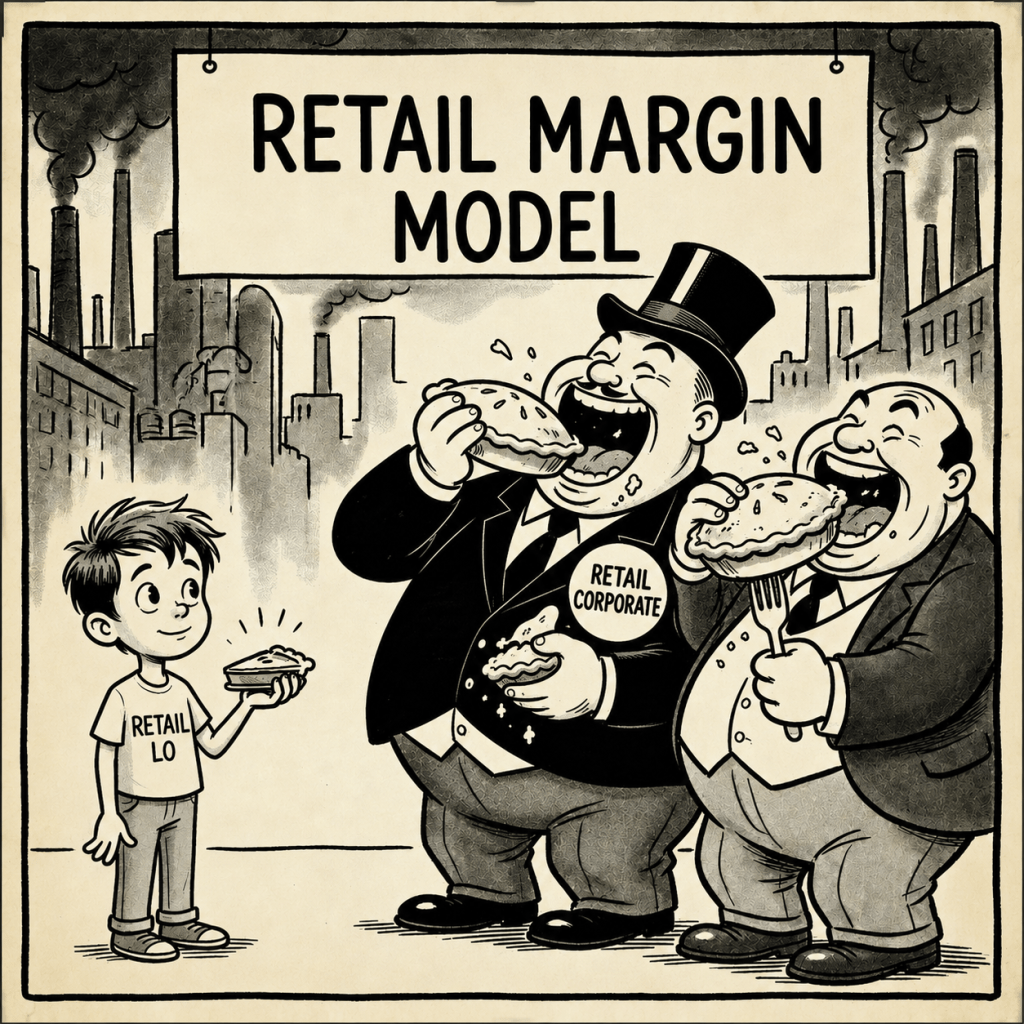

As I talk to retail lenders, there is a big misconception on how pricing works. The assumption is that lender margin is universal and the discrepancy comes from lender comp alone.

So if lender A pays their LOs 100 bps and lender B pays their Los 150 bps, then lender A will be 50 bps better on rate, right?

Maybe, if corporate margins are the same. But they aren’t.

This is where brokers shine.

For the most part, we don’t carry the over head that retail lenders do. Retail have offices, salaries, cumbersome production, compliance, HR departments, local management, middle management, and upper management/C suite positions, and often every office have receptionists/office managers, etc.

When you sell money, the only way to make money is margin.

In this case, the only way to pay salaries of non-producing roles, is higher margin.

So really it’s lender A pays their LOs 100 bps, their LOA 15 bps, their processor 20 bps, their BM 20 bps, SVP/regional VP 10 bps, corporate gets over 100 bps, etc. Lender B (broker) pays their LO 200 bps and uses a third party processor who is either paid by the buyer or LO separately.

Both close on time, both give good service.

Now you tell me which is the better model?

— Blake | BridgePoint Mortgage Chandler | NMLS# 1365524